Outputs From The LIC DSF Template

Welcome to Station 6! It will guide you through all the LIC DSF outputs that are automatically produced by the template once all the assumptions in the input sheets have been entered.

|

|

|

|

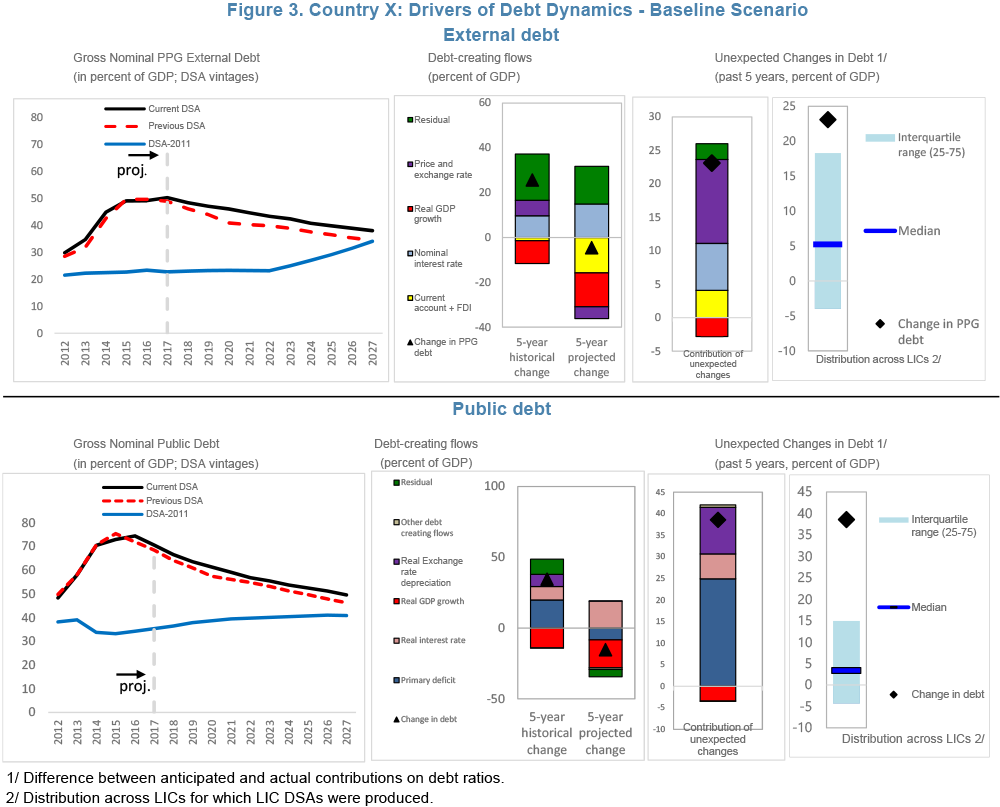

Baseline

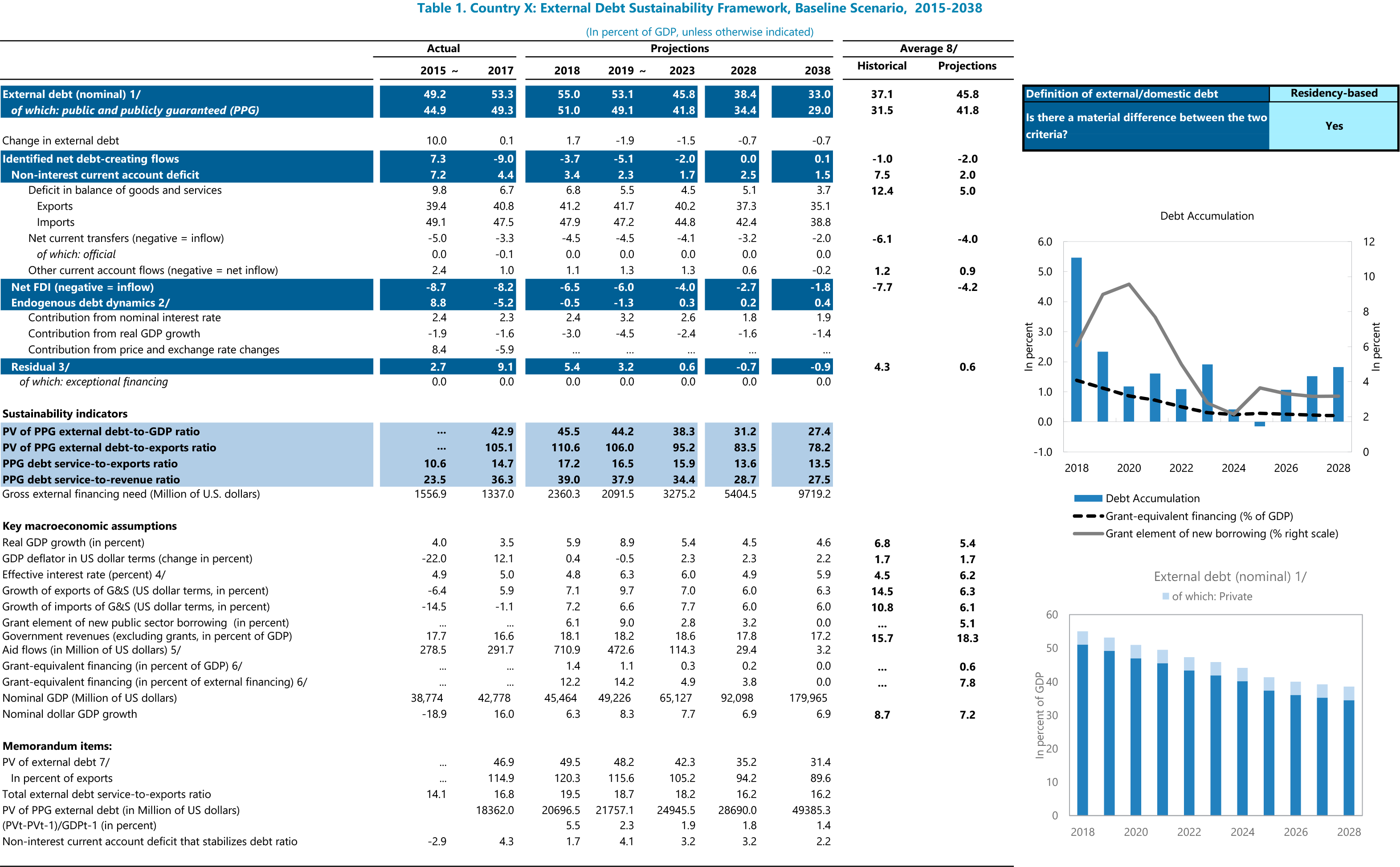

The "Output 1-1 - External DSA" sheet displays information under the baseline scenario of the external DSA.

In the template, this table is in the “Output 1-1” sheet.

|

|

|

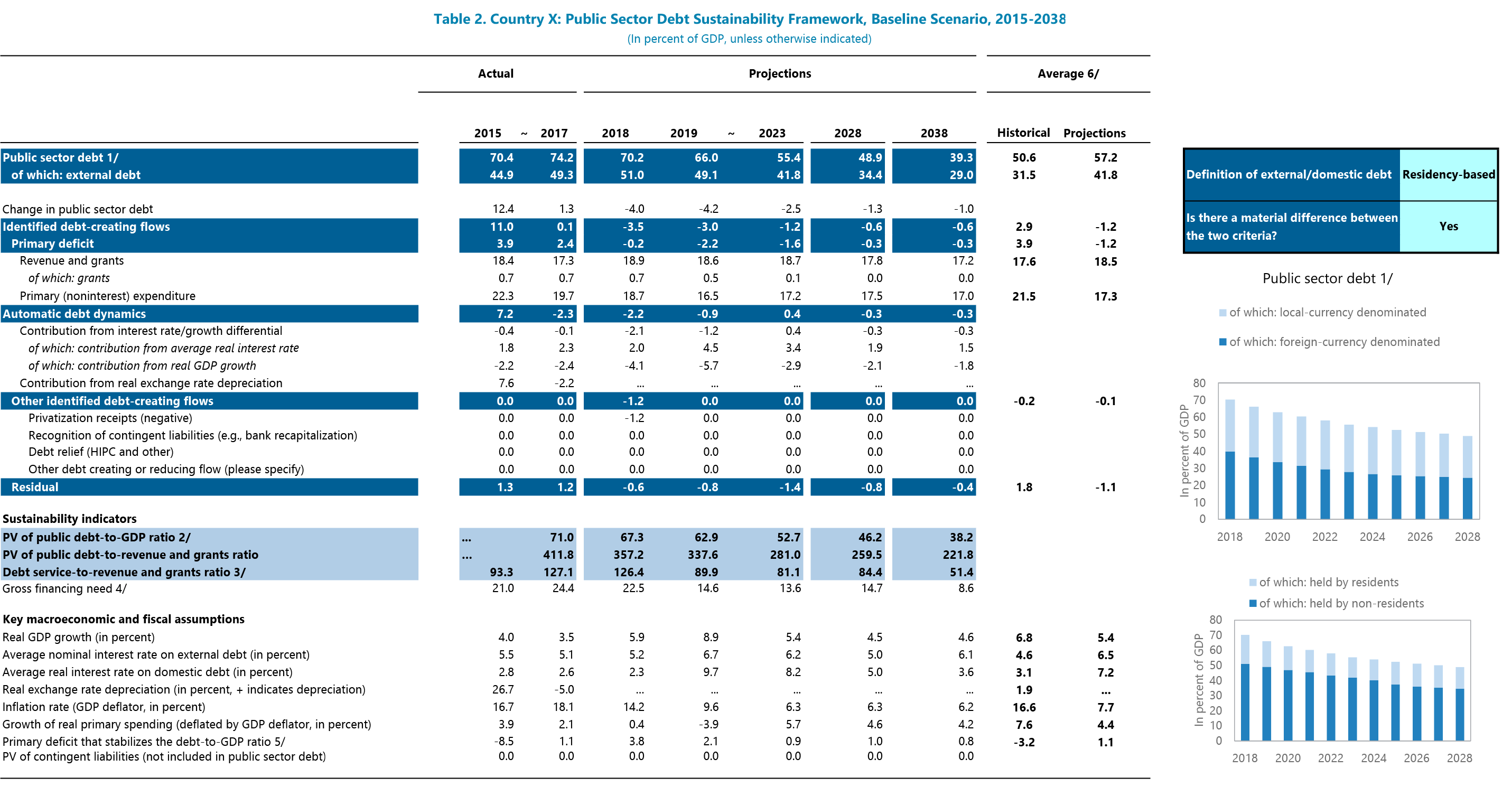

The Output 1-2 - Public DSA sheet displays information under the baseline scenario of the Public DSA.

In the template, this table is in the “Output 1-2 - Public DSA” sheet.

|

|

|

|

Key Messages

Key Messages

- Baseline projections for external and public DSAs are summarized in the respective External and Public Output 1 tables.

- For an external DSA, the output table summarizes the projections of the external debt-to-GDP ratios. It also decomposes its projected evolution (change in debt) into the main drivers of external debt dynamics: identified debt-creating flows less net FDI plus endogenous debt dynamics plus residual.

- For a public DSA, the output table summarizes the projections of the public debt-to-GDP ratios. It also decomposes its projected evolution into the main drivers of public debt dynamics: identified debt-creating flows plus automatic debt dynamics plus other flows plus residual.

- PPG external debt is part of the total external debt as well as part of the total public debt.

Baseline Stress Test Charts

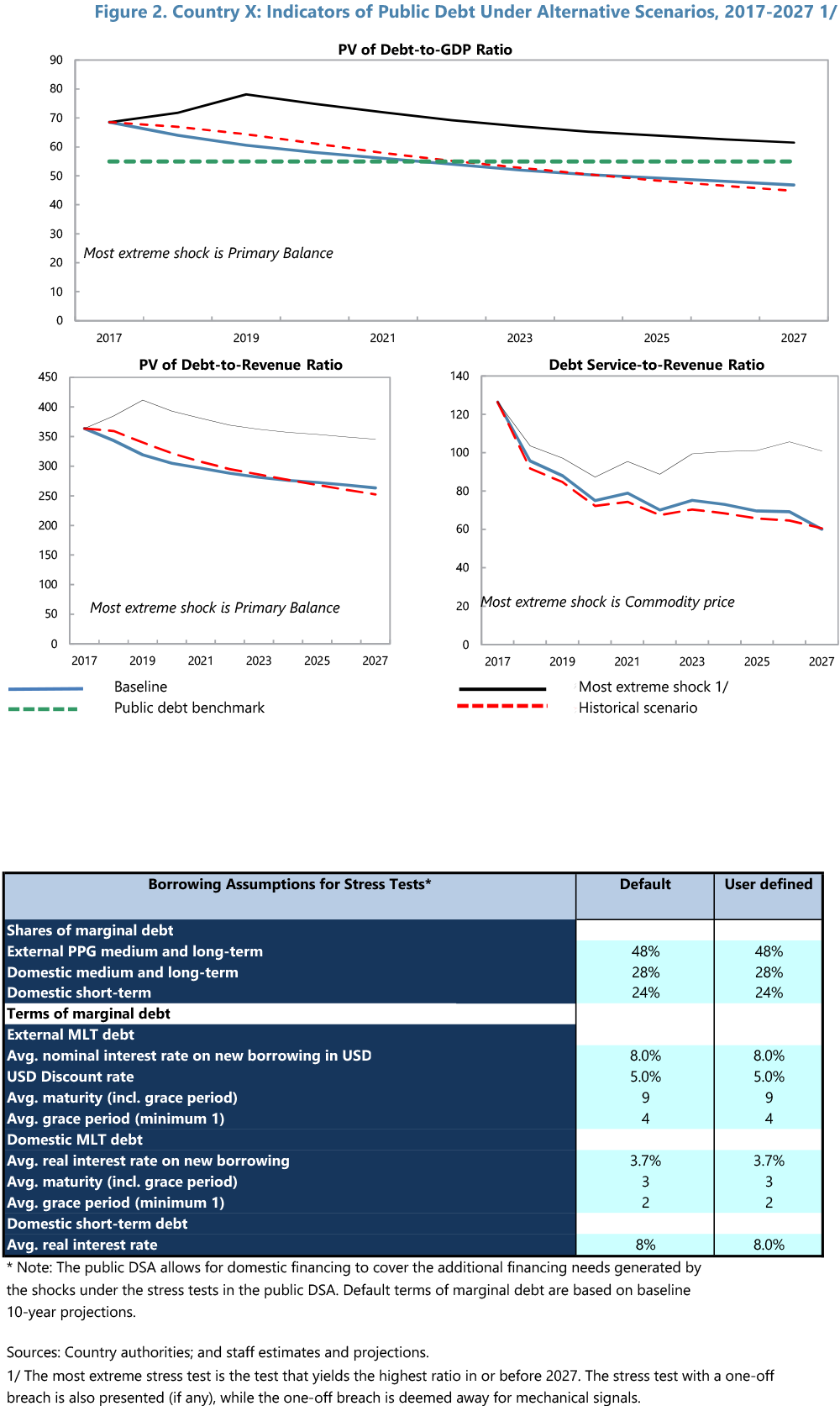

Output 2-1 - Stress_Charts_Ex shows relevant debt indicators for PPG external debt.

In the template, this table is in “Output 2-1” sheet.

|

|

|

|

Output 2-2

In the template, this table is in the “Output 2-2” sheet.

|

|

|

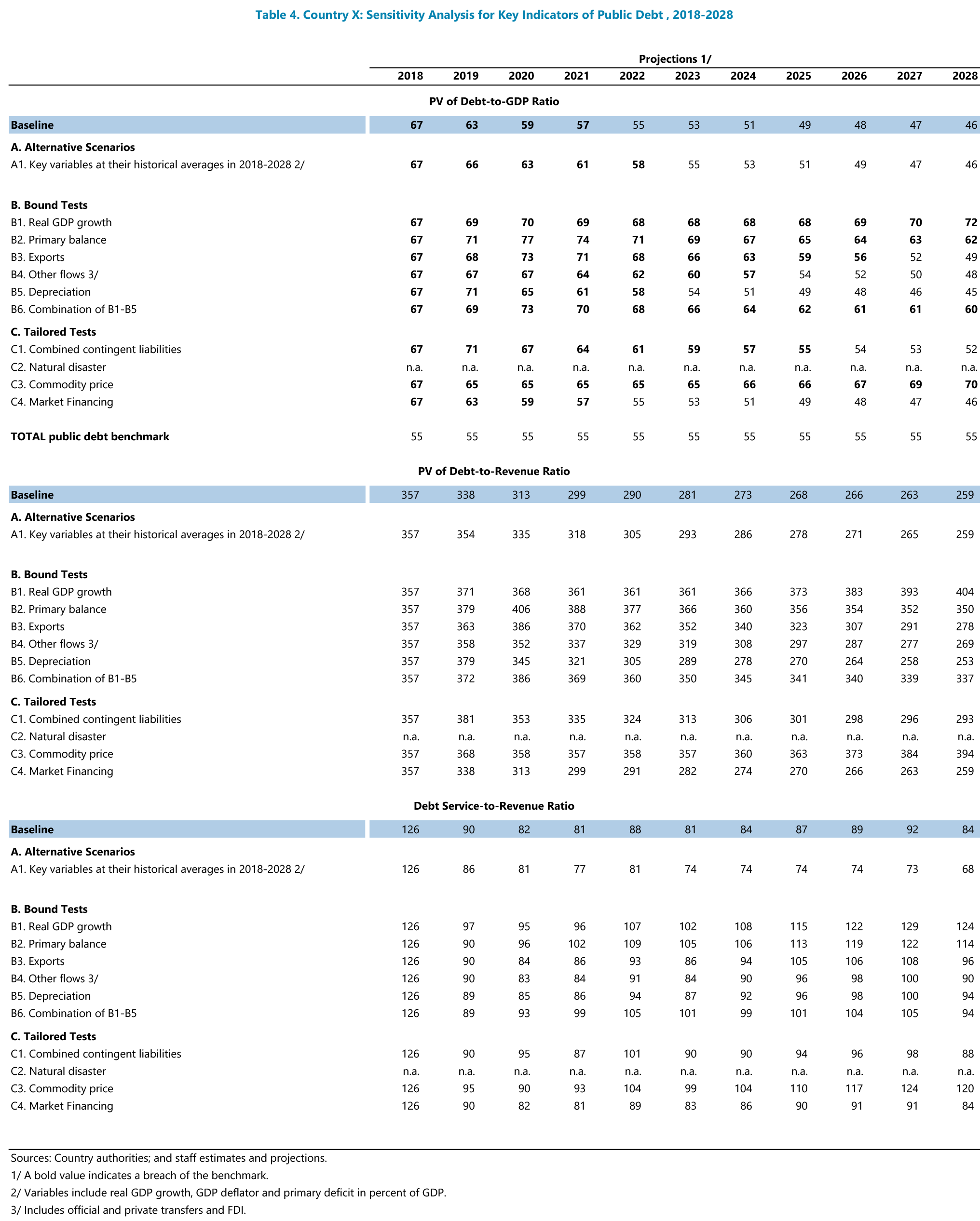

Output 3. External and Public Stress Tests Tables

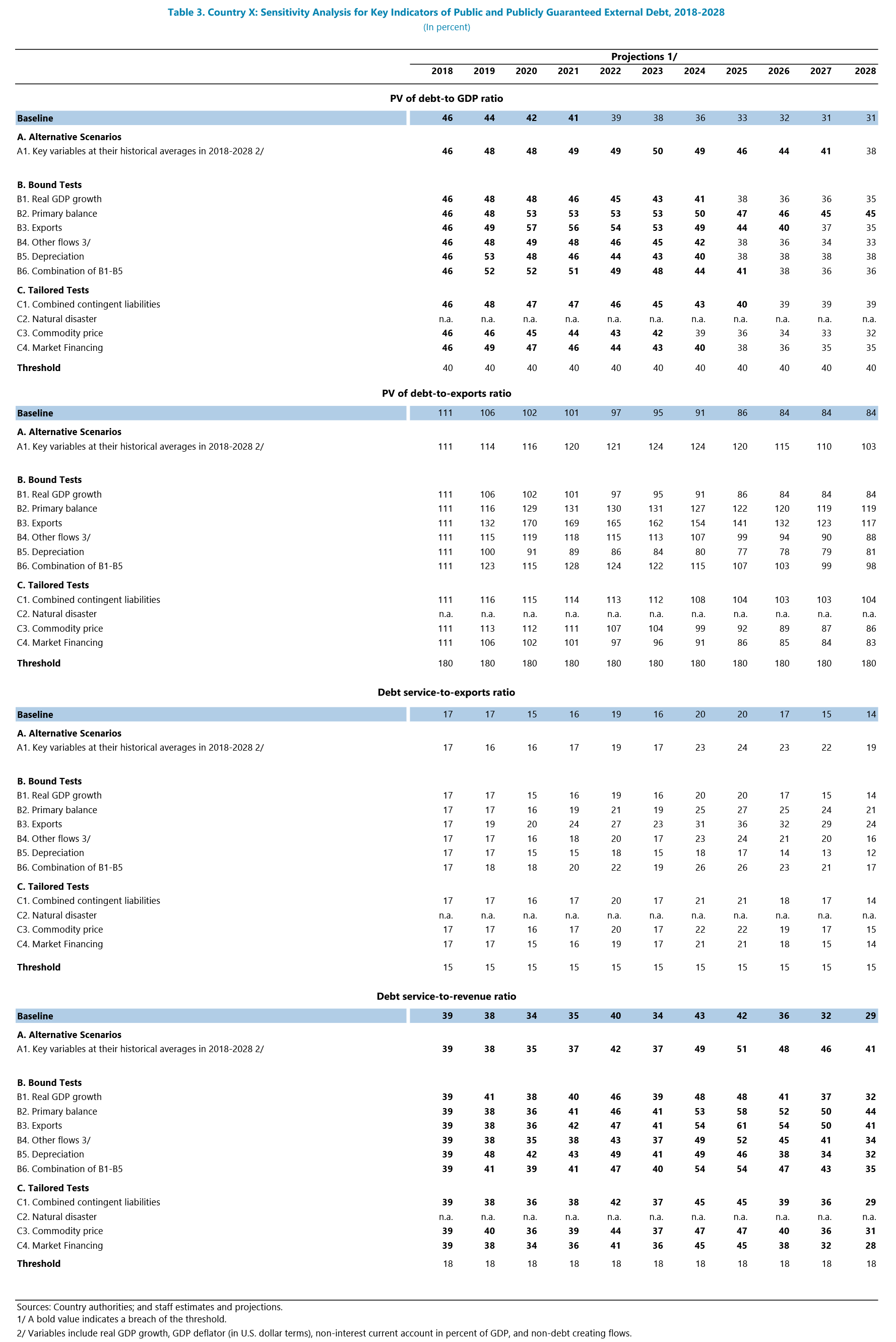

The "Output 3-1 Stress-External" sheet displays the values of the debt burden indicators under the external DSA under the baseline, the historical scenario, and each of the stress test scenarios. The thresholds are also shown.

In the template, this table is in the “Output 3-1" sheet.

|

|

|

|

The "Output 3-2 Stress-Public" sheet displays the values of the debt burden indicators under the public DSA. Like in the external DSA table above, the baseline, the historical scenario, each of the stress test scenarios, and the thresholds are shown.

In the template, this table is in the “Output 3-2” sheet.

|

|

|

|

Key Messages

- The projections of the key ratios for PPG external debt and public debt are plotted against their respective external debt thresholds and public debt benchmark (presented in Station 4). The respective output tables summarize the evolution of the ratios under the stress scenarios.

- The charts show the breaches under the baseline, if any, and the stress scenarios, which in turn determine the mechanical risk ratings under both the external and public DSAs.

Sensitivity Analysis

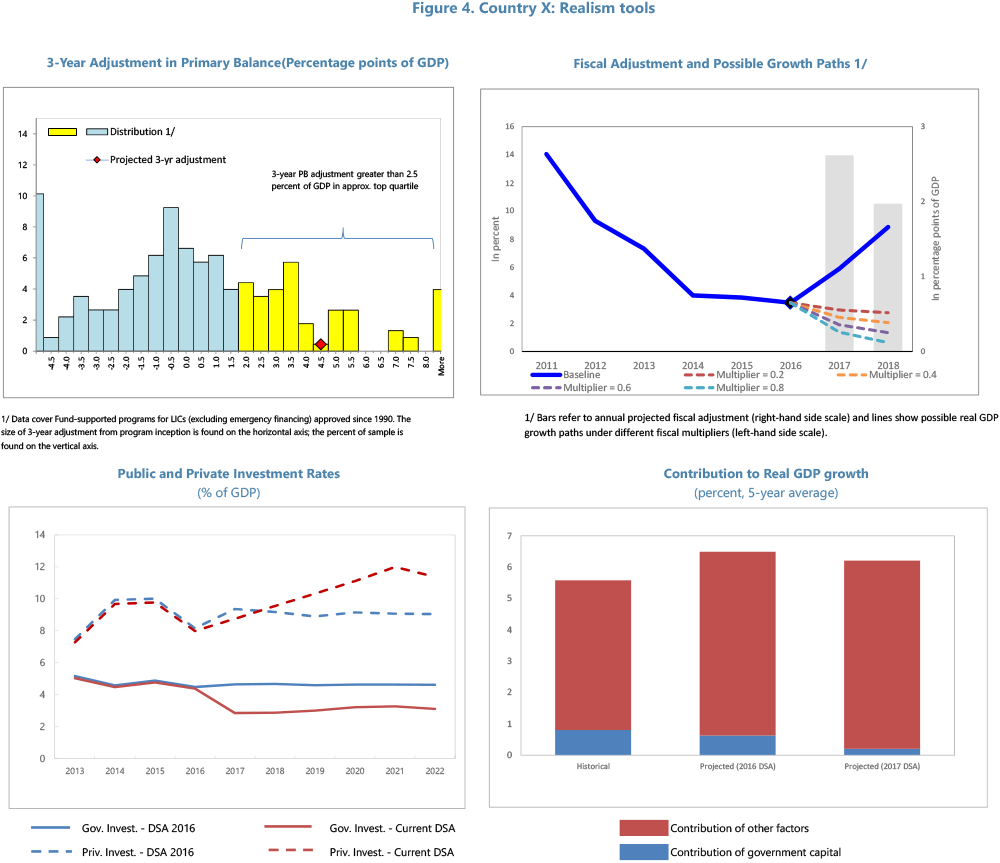

The "Output 4-1 - Forecast Error" sheet displays the output of the realism tools discussed in Station 3. This output is to be included in the report.

In the template, this table is in the “Output 4-1” sheet.

The "Output 4-2 - Realism" sheet also displays the outputs of the realism tools discussed in Station 3. This output is to be included in the report.

In the template, this table is in the “Output 4-2" sheet.

Key Messages

- The realism tools from Station 3 summarize the realism of the baseline macroeconomic and debt projections by comparing the projected evolution of debt and its underlying drivers to the historical outcome.

- The realism of the projected fiscal adjustment is evaluated relative to the historical data base of the past fiscal adjustments in LICs and with respect to the implied fiscal multiplier (i.e., the assumed impact of the projected fiscal adjustment on growth).

Risk Rating & Other Outputs

The charts below are included in this station to show the complete set of outputs of the LIC DSF. The contents of the charts will be discussed in detail in subsequent stations.

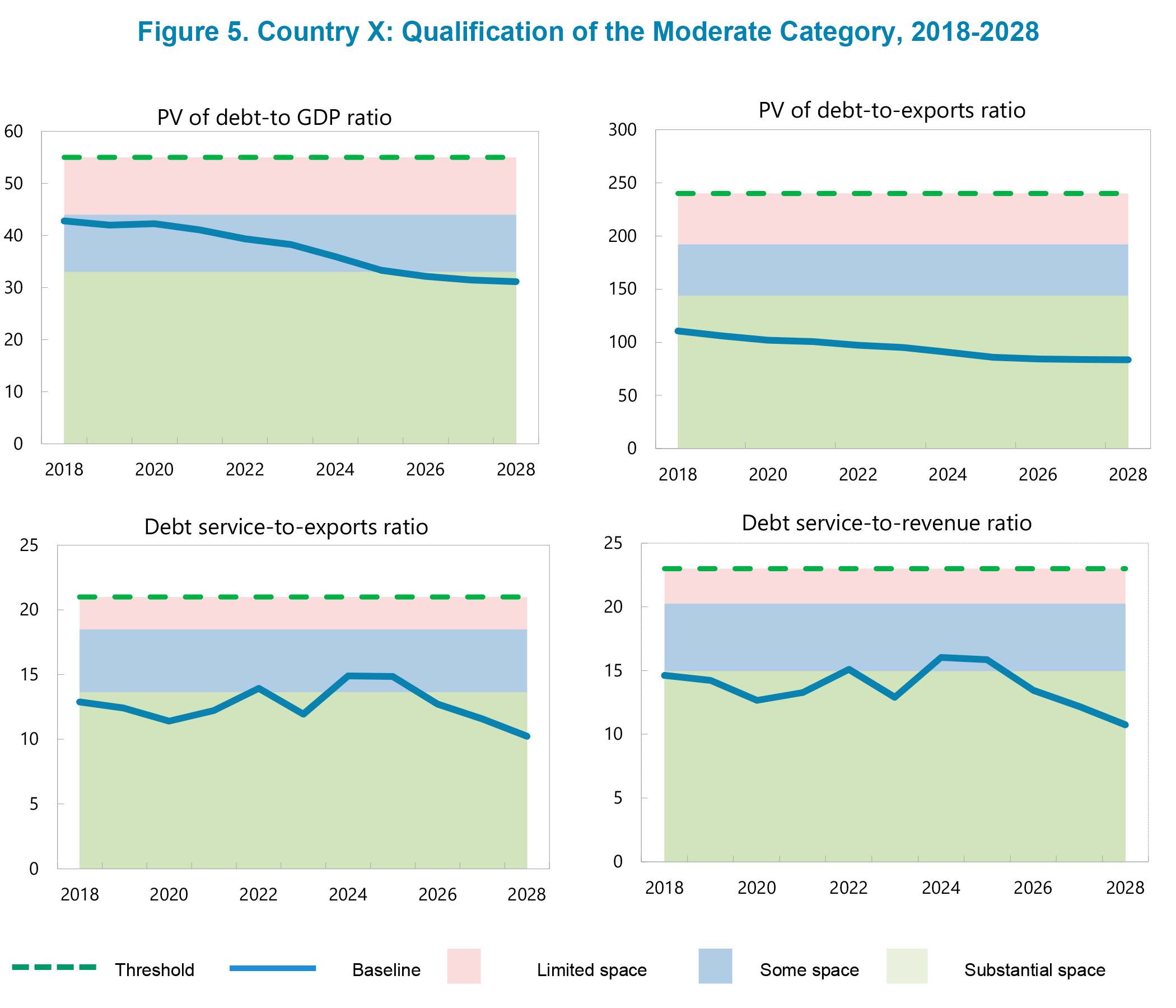

The "Output 5-1 Moderate risk" sheet is only for LICs rated at moderate risk of external debt distress. Please see detailed explanations in Station 9.

In the template, this table is in the “Output 5-1” sheet.

Output 5-1

The "Output 5-2 Market module" sheet shows the results of the market financing tool. This is only relevant for countries with market access. For reference, the panel charts show the external debt burden indicators under the market financing tailored stress test and the baseline scenario. Please see detailed explanations in Station 7.

In the template, this table is in the “Output 5-2” sheet.

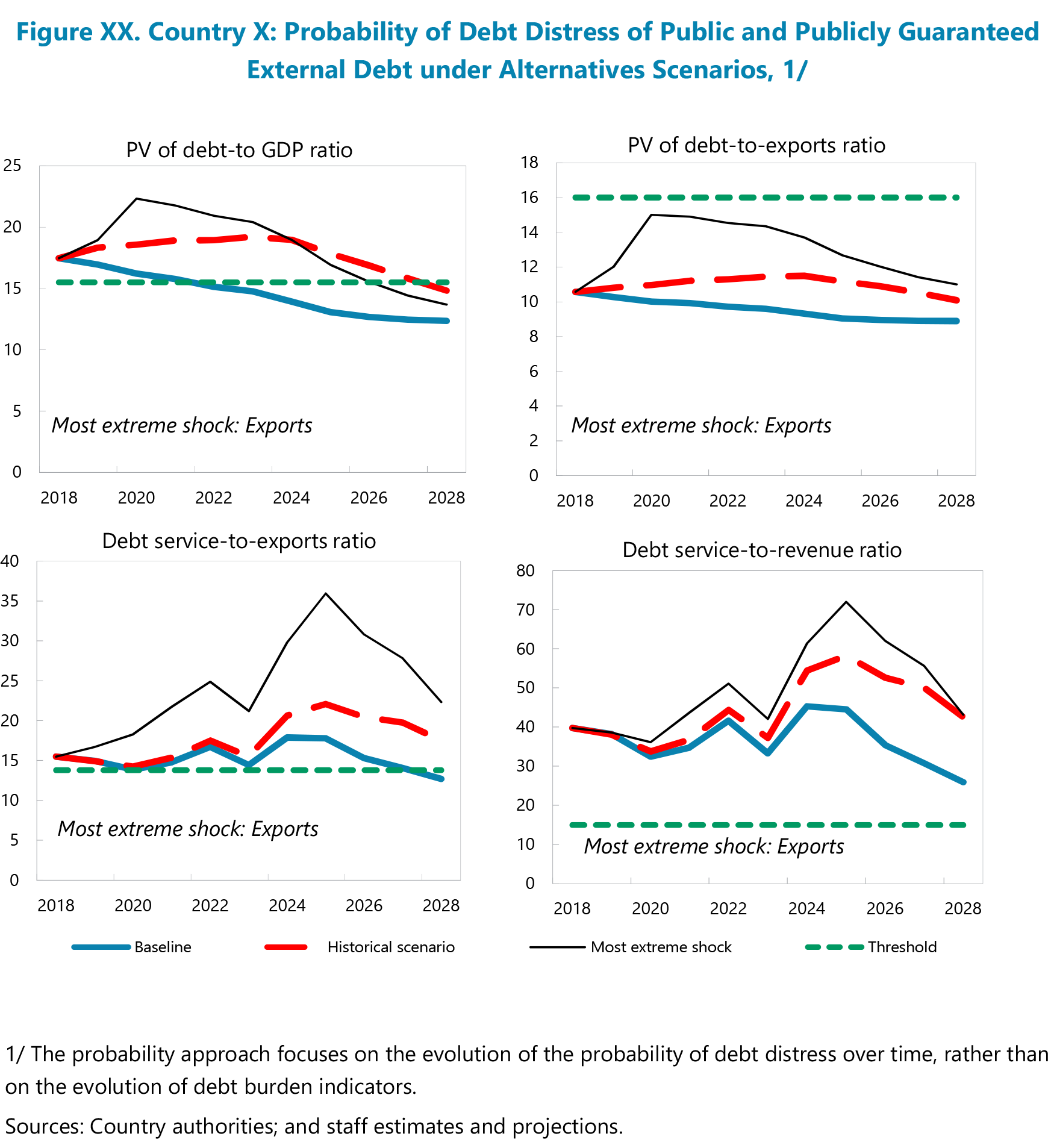

The "Output 6" sheet is optional and only to be included if the probability approach is used.

The probability approach may be used when a country’s risk rating is on the border between two categories under the traditional (threshold) approach. This is meant to enhance a case for assigning the final risk rating after all other factors informing judgement.

In the template, this table is in the “Output 6” sheet.

Key Messages

- The Moderate Risk and Market-Financing Risk modules, as well as the Probability Approach module, only apply to selected LICs and therefore do NOT inform the mechanical risk ratings.

The table below recalls how the mechanical external risk signal is determined based on the number of breaches under the baseline scenario (first column) and the stress scenarios (second column) for the four debt burden indicators. For further explanation, please see Station 9.

| Number of Breaches Under the Baseline Scenario |

Number of Breaches Under the Stress Scenario |

|

| 0 | 0 | |

| 0 | 1+ | |

| 1+ | 1+ |

The overall risk of public debt distress (low, moderate, or high) is derived based on joint information from the five debt burden indicators: the four from the external block, as explained above, plus the PV of total public debt-to-GDP, which is compared with its estimated indicative benchmark.

Single one-year breaches are automatically deemed away.

Final External Risk of Debt Distress

Occurs when the PPG external debt has a low risk signal (none of the PPG external debt burden indicators breach their respective thresholds under the baseline or the most extreme stress test) and judgement based on country-specific knowledge is applied.

Occurs when the PPG external debt has a moderate risk signal (none of the PPG external debt burden indicators breach their thresholds under the baseline, but at least one indicator breaches its threshold under the stress tests) and judgement based on country-specific knowledge is applied.

Occurs when any of the PPG external debt burden indicators breaches its threshold under the baseline and judgement based on country-specific knowledge is applied.

The final overall risk of public debt distress (low, moderate, or high) can also be different from the mechanical signals through judgement.

The external debt distress risk rating remains the primary DSF output, while the overall risk of public debt distress is considered supplementary information.

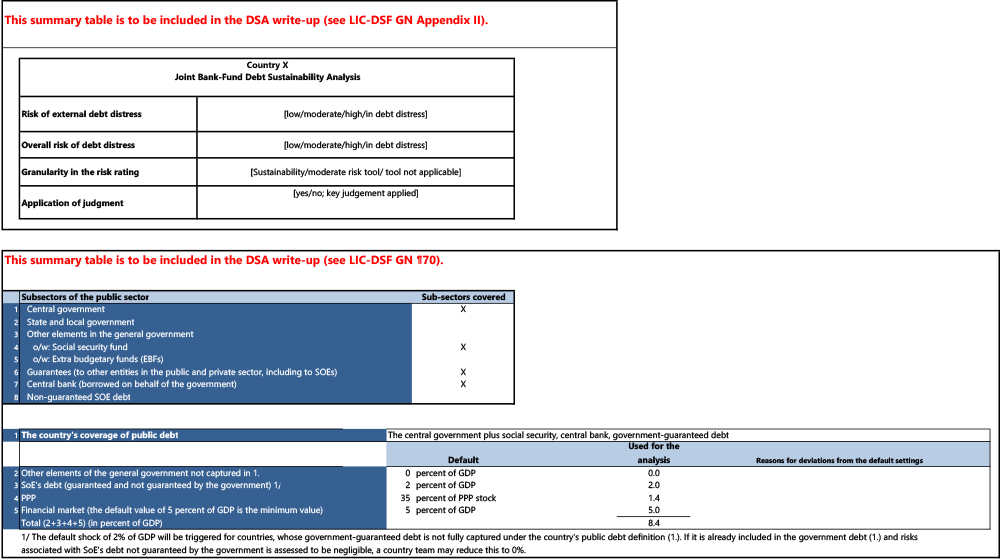

The "Output 7 - Risk Rating" sheet includes the final external and overall risk of debt distress ratings. It also provides granularity and insight into applications of judgement.

In the template, this table is in the “Output 7 - Risk Rating” sheet.

|

||

|

|

Takeaways for Station 6

Takeaways for Station 6

- Debt burden indicators under the baseline scenario determine the mechanical high risk signal; the stress test scenarios determine the mechanical moderate risk signal.

- A short-lived (one-year) breach for each debt burden indicator is automatically disregarded.

- Signals from the market financing tool are applied to the final risk rating through judgement.

Travel to Station 7 for the next part of your journey

|

|

|

|

|

|

|

|

|

|