Explore the report:

Services for Development: East Asia and Pacific Economic Update, October 2023

Services for Development

Most economies in developing East Asia and Pacific (EAP), other than several Pacific Island Countries, have recovered from the succession of shocks since 2020 and are continuing to grow, albeit at a slower pace. While the region will benefit from a recovery of the global economy in 2023, high indebtedness, a slowdown in China economy, and trade and industrial policy in other countries will hurt the region. Looking forward, diffusion of digital technologies and policy reforms in the services sector is posed to create opportunities and play an increasing role in the economic development of the region.

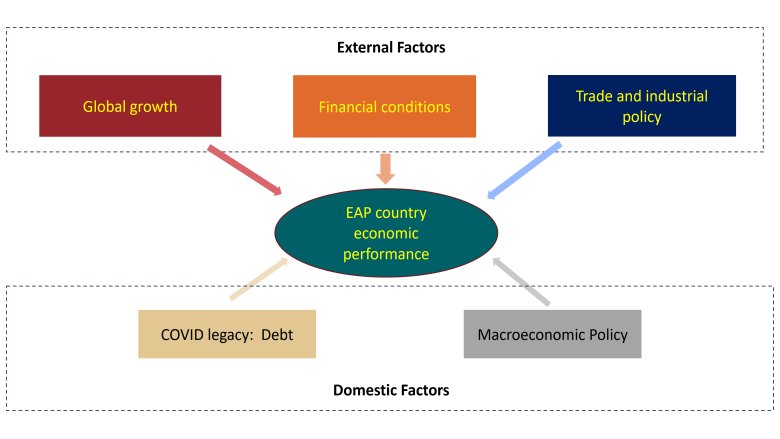

Most economies in developing East Asia and Pacific (EAP), other than several Pacific Island Countries, have recovered from the succession of shocks since 2020 and are continuing to grow, albeit at a slower pace. Economic performance in the region is being shaped by both external and domestic developments.

Read this section of the report:

Growth in the region remains higher than the growth projected in other emerging markets and developing economies, but is slowing compared to earlier projections. While growth in China is projected to slow, growth in the rest of the region is expected to edge up in 2024.

Read this section of the report:

Looking ahead to the medium and long term, the development of services will be central to EAP’s overall development. East Asia’s rapid economic growth in recent decades is often seen as driven by the manufacturing sector. Yet, services are playing a growing, but often underappreciated role as key drivers of economy-wide growth and job creation.

Read this section of the report:

Policy Issues examined in recent economic updates

Previous updates have focused on a number of other policy issues, including:

(1) Vaccination to contain COVID-19;

(2) fiscal policy for relief, recovery, and growth;

(3) climate policy to build back better;

(4) smart containment of COVID-19, especially through non-pharmaceutical interventions like testing-tracing-isolation;

(5) smart schooling to prevent long-term losses of human capital, especially for the poor;

(6) social protection to help households smooth consumption and workers reintegrate as countries recover;

(7) support for firms to prevent bankruptcies and unemployment, without unduly inhibiting the efficient reallocation of workers and resources;

(8) financial sector policies to support relief and recovery without undermining financial stability;

(9) trade reform, especially of still-protected services sectors—finance, transport, communications—to enhance firm productivity, avert pressures to protect other sectors, and equip people to take advantage of the digital opportunities whose emergence the pandemic is accelerating;

(10) creating opportunities for firms and ensuring inclusion to promote equitable growth;

(11) policies to encourage technology diffusion and adoption; and

(12) policies to address new and old distortions in the areas of food, fuel and finance.

(13) Policies to face up to the major challenges of de-globalization, aging and climate change

MULTIMEDIA

pagetitle_video

Watch the Report Launch Event