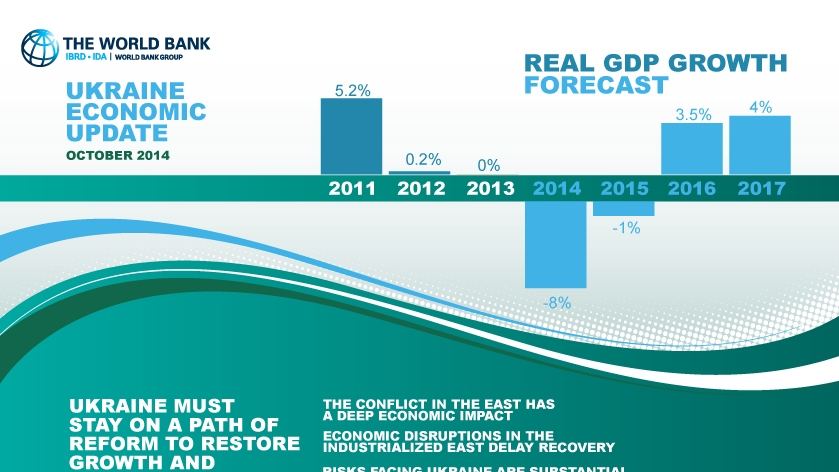

Kyiv, October 2, 2014 – Recent trends point to a sharper decline in real GDP in 2014 and a slower recovery in 2015 compared to earlier projections. In its recent Ukraine Macroeconomic Update, the World Bank projects real GDP to fall by 8 percent in 2014 and by 1 percent next year, down from 0 percent in 2013.

Conflict in the east is mainly responsible for these lower forecasts as it has disrupted economic activity, made collection of taxes difficult, adversely affected exports, and hurt investor confidence. Meanwhile, weak revenue performance, rising spending pressures and a growing Naftogaz deficit make fiscal adjustment more challenging. The current account deficit has adjusted because of the sharp depreciation, but balance of payment pressures remain high due to large external debt refinancing needs, low FDI, and limited access to external financing.

Real GDP, % change |

||||

2011 |

2012 |

2013 |

2014F |

2015F |

5.2 |

0.2 |

0.0 |

-8.0 |

-1.0 |

Risks to these forecasts are high and cannot be fully mitigated. A prolonged confrontation in the east, constrained credit supply due to risks in the banking sector, constrained domestic consumption, and investment demand all pose risks and affect prospects for recovery. Efforts to restore sustainable public finances could prove to be more challenging than expected, leading to a slower fiscal adjustment path than envisaged in the IMF SBA. Pressures are exacerbated by Naftogaz – a major fiscal risk.

“Ukraine is facing unprecedented challenges and risks,” said Qimiao Fan, Country Director for Belarus, Moldova and Ukraine. “The best way to deal with these challenges and risks is to continue macroeconomic adjustment and structural reforms.”

{kind=link}